Coming from a tech background, I’ve spent most of my career building and scaling digital products, guided by a formula I carried forward from my time at Adyen: launch fast and iterate. But building utility-scale solar plants feels entirely different – it is physical, grounded, and deeply integrated with regulations, infrastructure, and people.

In this piece, I want to share some of my observations and takeaways so far – from an outsider’s perspective. What once felt like a vast, complex industry from the outside now feels surprisingly small, with a handful of key players shaping most of the impact across the value chain. There’s a running joke we often hear in meeting rooms:

everyone knows everyone in India’s solar ecosystem

And while that’s mostly true, a lot of that knowledge still stays behind those meeting room doors. At GIGA, we want to take a fresher approach in sharing first-hand experiences as they are: honest and transparent.

First, the macros

One of the first things I tried to understand when I entered the space was just how big India’s energy ecosystem really is. As of August 2025, India’s total installed power generation capacity stands at around 495 GW. Out of this, about 243 GW (nearly 49%) comes from renewable sources like solar, wind, and hydro. Solar alone contributes close to 123 GW, a share that continues to grow faster than any other source. (Source: NITI Aayog, India Climate & Energy Dashboard)

The government has set a target of 500 GW of non-fossil-fuel capacity by 2030. Initiatives like PM-KUSUM, which focuses on helping farmers solarise irrigation and generate income from their land, and PM Surya Ghar Muft Bijli Yojana, designed to make rooftop solar more accessible for households, are all aimed at pushing solar deeper into both rural and urban India.

Getting jargons out of the way

Like every sector, solar comes with its own set of jargon. These terms play a big role in how projects are built, approved, and even priced. Let me break down a few of the important ones:

PPA (Power Purchase Agreement): A long-term contract between a power producer and a buyer (like a utility or company) that defines how much electricity will be sold, at what price, and for how long.

ALMM (Approved List of Models and Manufacturers): A list published by the Government of India that includes solar panel brands and models officially approved for use in government-backed projects. It’s part of India’s broader push to reduce dependence on imported modules.

DCR (Domestic Content Requirement): A policy that mandates solar developers to use modules and cells made in India for certain projects.

CUF (Capacity Utilisation Factor): Think of CUF as a solar plant’s report card. It shows how much electricity the plant actually generated compared to how much it could have generated if the sun shone perfectly all year. A higher CUF means the plant is performing more efficiently and making better use of its installed capacity.

The vacuum & the opportunity

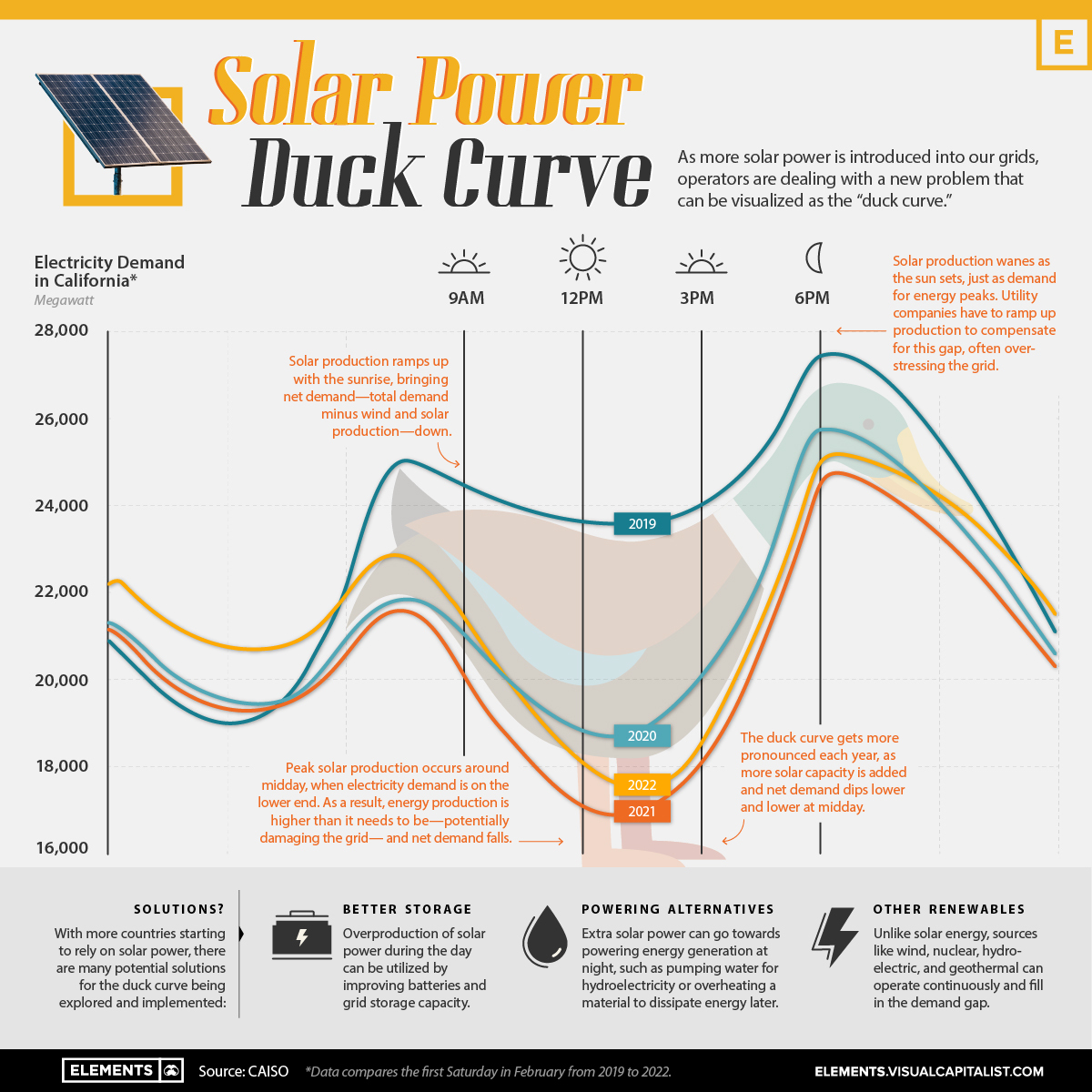

What stands out to me as the biggest gap is that most fixed-tilt solar plants operate at full capacity for barely three to four hours a day, depending on location and weather. The rest of the time, generation dips even as demand fluctuates – the classic duck curve problem. To bridge that gap, Battery Energy Storage Systems (BESS) feel less like an option and more like an eventuality. They’ll allow us to store the excess energy generated during the day and release it when demand peaks, creating long-term grid stability and reliability.

As I got onboarded at GIGA, Parth shared a really interesting paper from the Beckn Foundation, co-founded by Nandan Nilekani and Pramod Varma – the same people behind UPI. It talked about a Digital Energy Grid: a future where electricity could move as freely as money does today, enabling peer to peer energy exchange between homes, businesses, and communities. The idea felt futuristic, but it also made perfect sense. If open networks can transform finance, they can just as easily reshape how we produce and consume energy.

The future of this sector feels wide open, and I’m genuinely excited to see and contribute to how it unfolds – as an insider. A sequel to this blog titled “Solar from an Insider’s Perspective” already feels inevitable.